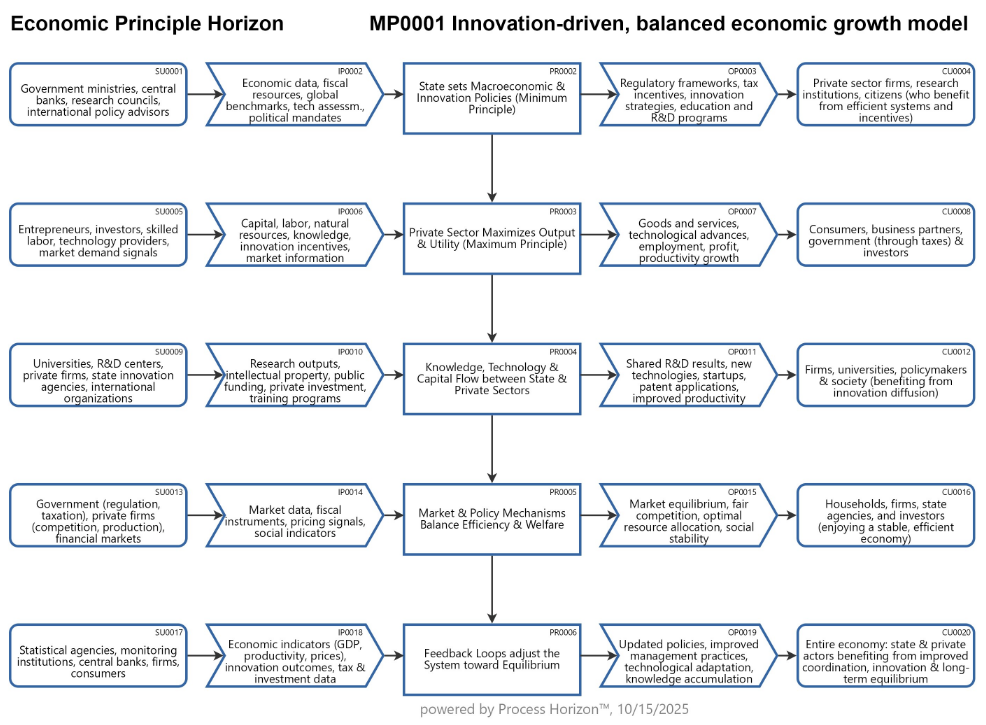

Innovation-driven, balanced economic growth model

In a balanced state–private economy, the value stream aligns public efficiency (minimum input) with private productivity (maximum output) through innovation, governance & feedback loops, achieving a dynamic equilibrium where economic and social returns are maximized with minimal resource use.

The equilibrium f(minInput) = f(maxOutput) represents the point where economic efficiency & social welfare are jointly optimized.

Innovation-driven economic growth can be enabled by investing in human capital, R&D, infrastructure, open markets & smart governance that promote creativity, risk-taking & knowledge diffusion. f(minInput) ↑Knowledge, f(maxOutput) ↑Knowledge meaning more output from less input, powered by iterative knowledge & ideas as growth driver rather than resources.

Tariffs distort the economic minimum & maximum principles by breaking the efficiency link between input & output.

- Under the minimum principle, tariffs raise input costs (especially imported materials), so producers can no longer achieve a given output with the minimum possible input cost. Efficiency falls & production shifts to higher-cost domestic resources.

- Under the maximum principle, tariffs raise consumer prices & limit output or utility for a given level of income or resources. Consumers & firms can no longer reach the maximum output or welfare from available inputs.

Using the following link you can access this sandbox SIPOC model in the ProcessHorizon web app and adapt it to your needs (easy customizing) and export or print the automagically created visual AllinOne SIPOC map as a PDF document or share it with your peers: https://app.processhorizon.com/enterprises/p6qJk98vousJJHNVBHhUtyHt/frontend